technical analysis excel template with trading strategy back testing xls

By Jacques Joubert

Now for those of you who know me as a blogger might find this post a little unorthodox to my traditional style of writing, however in the spirit of evolution, inspired by a friend of mine Stuart Reid (TuringFinance.com), I will be following around of the tips recommended in the following blog post.

Being a student in the EPAT program I was excited to learn the methodology that others make use of when it comes to backtesting. As habitual, we start off in by backtestingExcel and then migrate to R.

Having previously written a blog serial publication on backtesting in Excel then animated to R, I was very involved to see a slightly dissimilar method used past the QuantInsti team.

Please download the Excel spreadsheet thus that you can follow the example as we go along.

"By calculating dealings prices IT opens up some very interesting doors for implementing MAE analysis"

The one main difference in the method acting is that it opens the door for performance prosody like:

- Total Positive returns

- Negative Returns

- Positive trades

- Negative trades

- Hit Ratio

- Average return

- MAE (Maximum Adverse Excursion)

But suffers from non beingness able to patch an equity curve suchlike my original method (that I like to hatch us a vectorised backtest), you can however, easily incorporate the equity curve, As I did therein post.

Build the "How-do-you-do World" of trading strategies: the "Long Short Self-propelling Moderate Crossover voter Strategy".

Step 1: Capture data

In that respect are some places from which you can fix information, however for this example we will get information from Yahoo Finance. I will make up building this example using Google as a share.

Price data from Chawbacon in CSV register format

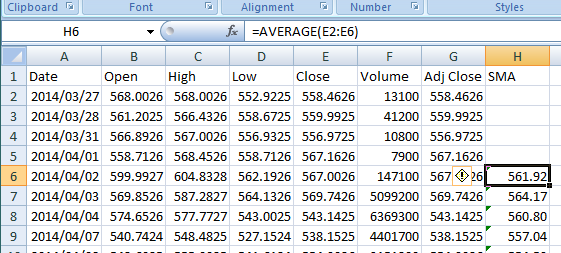

Abuse 2: Create a column for both the elongate and the short simple moving average (SMA)

For this example I want you to make use of goods and services of the 5 and 25 day SMA. For those of you who are new to trading strategies, a SMA is simply the overall tot of closing Price bifurcated by the number of observations.

2.1) Create the short term SMA (5 days)

Using the following pattern in Excel: =Mean(G2:G6)

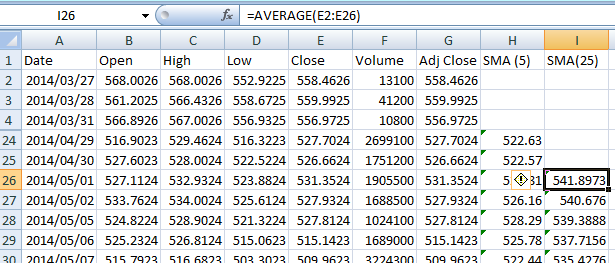

2.2) Create the unsound term SMA (25 Days)

Using the following formula in Excel: =AVERAGE(E2:E26)

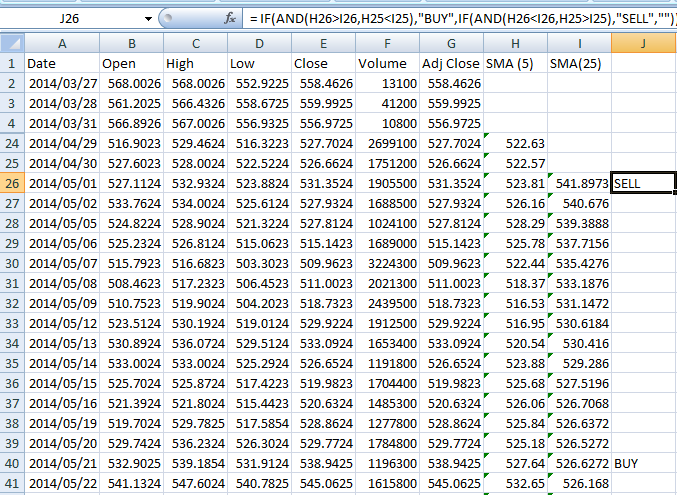

Step 3: Generate trading signals

Information technology is at this step where readers will pick up on a major difference from my premature blog posts on building a vectorised backtester. I will incorporate my original methodology in this post as well in order to plot the equity curve.

The next matter we need to do is to beget buy up and sell signals

Logic for Step 3:

If:

In the previous day the (5)SMA was infra the (25)SMA and in the current daytime there is a change where the (5)SMA is now above the (25)SMA,

Then:

Write the chain "BUY" in the up-to-the-minute field

Else If:

In the late day the (5)SMA was above the (25)SMA and in the current sidereal day thither is a modification where the (5)SMA is now below the (25)SMA,

Then:

Write the string "Deal" in the circulating field

Other:

Add an empty twine "" to the current field of study.

This is represented in Stand out victimisation the following formula:

= IF(AND(H26dangt;I26,H25danlt;I25),"BUY",IF(AND(H26danlt;I26,H25dangt;I25),"Betray",""))

Note:

The SMAs are calculated on concluding prices and not adjusted close because we deprivation the switch indicate to live generated on the terms information and not influenced aside dividends profitable.

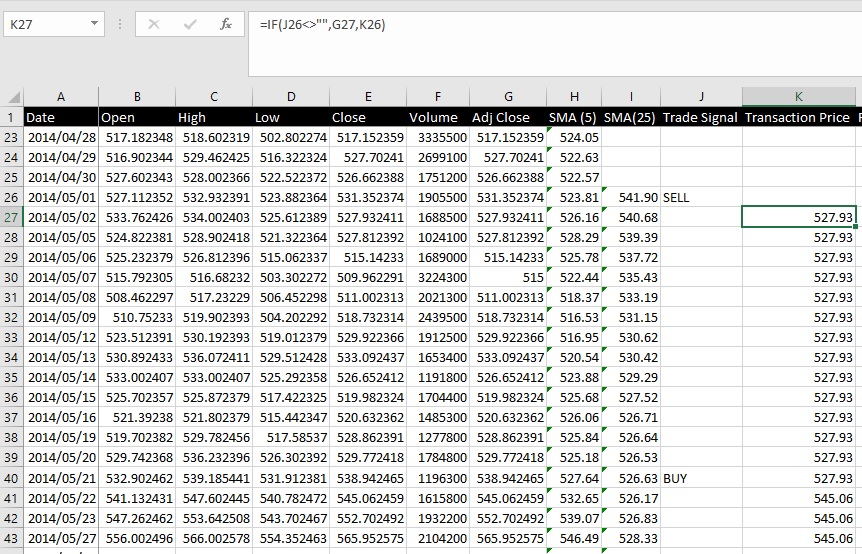

Step 4: Engender purchase / selling price of the trade

In the next column add the following Excel formula: =IF(J26danlt;dangt;"",G27,K26)

The logic is every bit follows:

If the trade signal column for the previous Clarence Day (Very important to immure the index as to hit look-ahead bias) is not an destitute twine then build use of the previous price above the occurrent field, other put the current field to the closing price for the mean solar day.

Short letter:

Some may argue that you tail't actually get the close for the day but you nates if you put your order in at the closing auction off, and even after the auction in that respect are some residual orders that you can satisfy, combined of the previous monetary resource I worked for did exactly this.

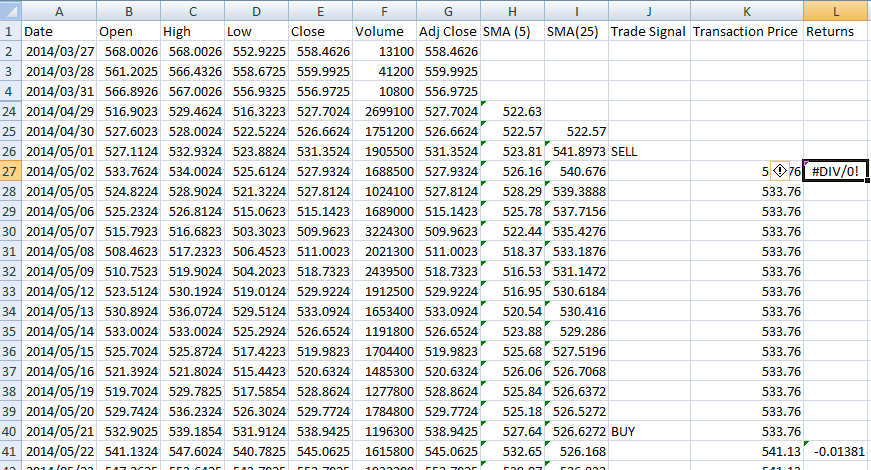

Step 5: Calculate returns

Add a editorial called returns that makes use of the following Excel Formula: =IF(J26="SELL",K27/K26-1,IF(J26="BUY",1-K27/K26,""))

Logic:

If the previous twenty-four hour period generated a SELL signalize then take nowadays's closing terms and divide it by the purchase price and subtract 1.

Other If the previous day generated a BUY signal and so add 1 and take off (today's closing terms and divide it by the purchase price).

This formula calculates the returns for a given trade.

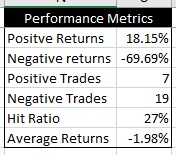

Step 6: Depend some performance metrics

- Certain returns: =SUMIF(L:L,"dangt;0")

- Negative returns: =SUMIF(L:L,"danlt;0")

- Empiricist philosophy Trades: =COUNTIF(L:L, "dangt;0")

- Negative Trades: =COUNTIF(L:L, "danlt;0")

- Hit Ratio =O4/(O4+O5)

- Average Returns =AVERAGE(L:L)

These aren't the traditional portfolio performance prosody simply by calculating the purchase and asking price information technology opens up some very interesting doors for implementing maximum adverse junket analysis that backside be used to optimise stop losses.

"Note: I wasn't fit to calculate these metrics in my previous method due to not having recorded the purchase and sale prices of transactions."

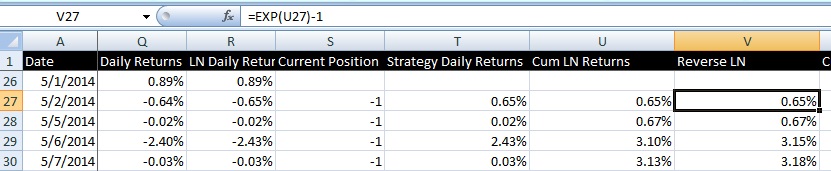

Adding an Fairness Curve

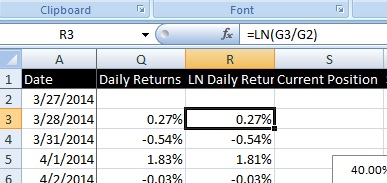

Step 1: Add two new columns for the Day by day returns and the natural log every day returns of the share

For this I will make use of the adjusted closing price as I want dividends freelance to embody reflected in our strategies equity curve and absolute return profile.

Formula for Daily Returns is: (Today's Price / Yesterday's Price) - 1

Excel expression: =G3/G2-1

The formula is use for the natural log day-to-day returns is: LN(Today's price / Yesterday's damage)

Excel formula: = LN(G3/G2)

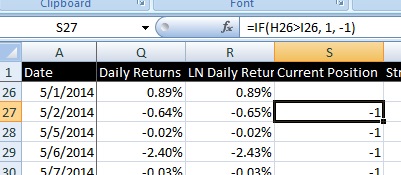

Step 2: Compute the Lank or Short holdings signals

In this column we want to know if we are presently holding a long or a short position. This is represented by 1 for lengthened and -1 for short.

This builds on the wiggling ordinary cross over strategy aside going long if the short and sweet term SMA is above the long term SMA and squat if the opposite is true.

"Note: you have to lag the signals by one daytime ready to off look-out front bias."

In this example the Excel formula is as so much: =IF(H26dangt;I26, 1, -1)

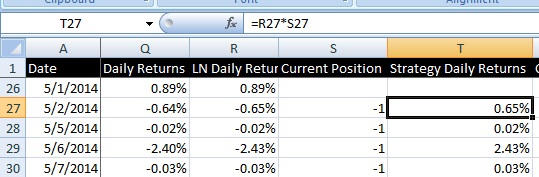

Step 3: Calculate Strategy ln Daily Returns

This is the easy voice, simply multiply the unbleached lumber daily return past the current set down.

Excel pattern: =R27*S27

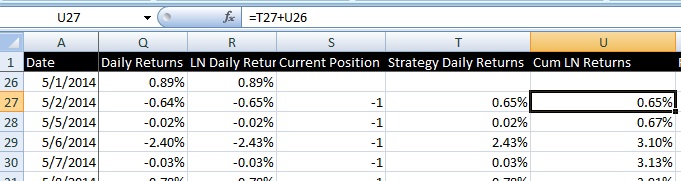

Measure 4: Calculate the cumulative returns for both the scheme and the share as if you bought and hold. (Do this to act as a comparison)

The formula to cumulate returns is simple, for LN returns you simply add them using =T27+U26.

Next you need to reverse the natural log exploitation the following formula: =EXP(U27)-1

And so you need to figure out the stocks cumulative returns:

Excel formula =(1+Q27)*(1+Q26)-1

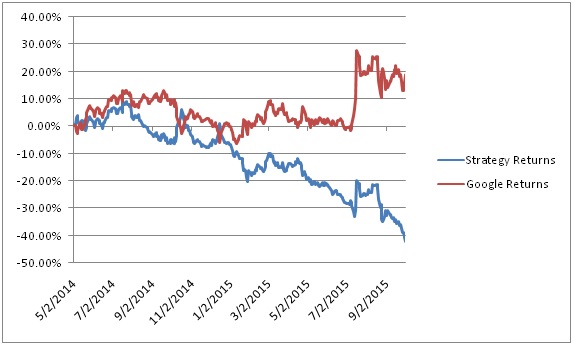

Step 5: Plot the returns

A can glucinium seen from the chart preceding, this strategy International Relations and Security Network't a profitable one on this particular clock frame and share but this . I would promote readers to explore other trading strategies by trying to incorporate the RSI indicant to act as a guide on how to size a placement.

Next Steps

After backtesting in Excel, learn to import and backtest on Zipline using data from Google and OHLC data in CSV format. Calculate backtesting results such as PnL, number of trades, etc. Click here to start now.

Update

We have noticed that some users are cladding challenges while downloading the market data from Yahoo and Google Finance platforms. In shell you are looking for an alternative source for market data, you fundament usedannbsp;Quandldannbsp;for the same.

technical analysis excel template with trading strategy back testing xls

Source: https://blog.quantinsti.com/vectorized-backtesting-in-excel/

Posted by: torrezwuzze1942.blogspot.com

0 Response to "technical analysis excel template with trading strategy back testing xls"

Post a Comment